Commission Treads Thin Ice with the European Semester

Adelina Marini, May 20, 2015

The big news from the presentation of one of the most important stages of the European semester - the country-specific recommendations (CSR) - is that France, Croatia, Finland and Britain will not be punished. Moreover, Poland exits the excessive deficit procedure earlier than planned. Another big news is that the Commission is giving up on a key obligation - applying the agreements - and leaves this in the hands of the member states. The changes this year could seem small at first sight but they are considerable in the context of the discussed possible changes of the Union's economic governance only 4 years after the big reform. In their conclusions last week the EU finance ministers (ECOFIN) recommend the Commission to focus the CSRs on areas that have macro-economic significance and where urgent actions are needed. This, according to the ministers, will give them more visibility in the national political discourse in the member states.

The big news from the presentation of one of the most important stages of the European semester - the country-specific recommendations (CSR) - is that France, Croatia, Finland and Britain will not be punished. Moreover, Poland exits the excessive deficit procedure earlier than planned. Another big news is that the Commission is giving up on a key obligation - applying the agreements - and leaves this in the hands of the member states. The changes this year could seem small at first sight but they are considerable in the context of the discussed possible changes of the Union's economic governance only 4 years after the big reform. In their conclusions last week the EU finance ministers (ECOFIN) recommend the Commission to focus the CSRs on areas that have macro-economic significance and where urgent actions are needed. This, according to the ministers, will give them more visibility in the national political discourse in the member states.

Basta reforms!

Done! The member states are tired of being mentored and the Commission is tired of being the bad cop. This is how the outcome of the functioning of the European semester can be summarised. Against the backdrop of the great ambition during the upgrade of the Stability and Growth Pact the implementation of the CSRs is very low. That is why the Commission has radically changed its approach as this year it presented a tangible modification of the recommendations. They are now much more concise, more specific and aim to resolve problems that can deliver quickly. As Vice President Valdis Dombrovskis (Latvia, EPP) explained after the ECOFIN meeting last Tuesday (12 May), this year's recommendations focus on "key macro-economic and social priorities that need to be addressed by each Member State in the coming year, to year and a half".

For the Commission, said Mr Dombrovskis a day later when presenting the recommendations, it is very important to foster the so called national "ownership" of reforms and implementation, which means the member states to start perceiving them as their own not as imposed from the outside. This is entirely in harmony with the new line of Jean-Claude Juncker's Commission. The problem is, however, that with the "return" of the ownership of reforms to the member states it is practically treading very thin ice which is reflected in the concern expressed by members of the Commission and by Eurogroup chief Jeroen Dijsselbloem. EU Commissioner for social affairs Marianne Thyssen (Belgium, EPP) underscored during the presentation of the CSRs that it is necessary to make full use of the nascent growth for reforms. "Member States should profit from the momentum and deliver on structural reforms", she said.

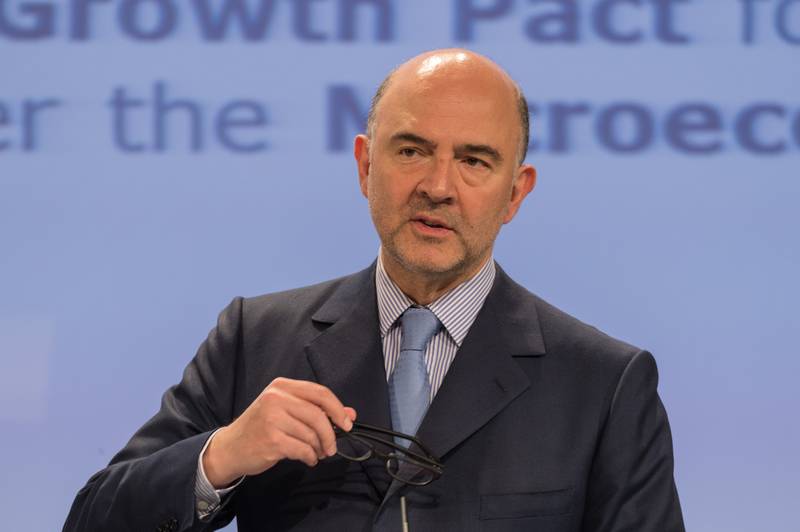

And Jeroen Dijsselbloem, the Dutch finance minister and Eurogroup chief (Socialists and Democrats), who is seeking a second term, said that "we all realise that we cannot keep counting on low energy and oil prices, quantitative easing and a low exchange rates. To keep the recovery on track, we need more investments, jobs and raising productivity". EU economic affairs Commissioner Pierre Moscovici (France, Socialists and Democrats) was not an exception. "Today we ask Member States to ensure that the ongoing economic recovery is more than a seasonal phenomenon. [...] These recommendations are not about Brussels lecturing governments. They are about encouraging national efforts to deliver the jobs and growth that we collectively need", he said.

The 2015 European semester - a Christmas for non-reformers

According to the spring economic forecast, there will be growth for everyone with the exception, probably, of Greece. In some member states growth could be more dynamic whereas in others it will remain anaemic. And as the variety of cases in EU is today really big the Commission decided to be generous to everyone. In this way, the countries that are almost at the highest alert level - fifth (out of 6) - will not be punished. In this group are Bulgaria, Croatia, France, Italy and Portugal. Last year on this level were only three countries - Croatia, Italy and Slovenia. The latter managed to go several steps down but her place was quickly taken by three new countries - France, Portugal and Bulgaria. The Commission was benevolent to other countries as well which are not in such a dire situation but, still, are in violation of the rules. Poland will be taken early out of the excessive deficit procedure and Britain will get two more years to correct its excessive budget deficit. And the Council will decide about Finland's violations.

According to the spring economic forecast, there will be growth for everyone with the exception, probably, of Greece. In some member states growth could be more dynamic whereas in others it will remain anaemic. And as the variety of cases in EU is today really big the Commission decided to be generous to everyone. In this way, the countries that are almost at the highest alert level - fifth (out of 6) - will not be punished. In this group are Bulgaria, Croatia, France, Italy and Portugal. Last year on this level were only three countries - Croatia, Italy and Slovenia. The latter managed to go several steps down but her place was quickly taken by three new countries - France, Portugal and Bulgaria. The Commission was benevolent to other countries as well which are not in such a dire situation but, still, are in violation of the rules. Poland will be taken early out of the excessive deficit procedure and Britain will get two more years to correct its excessive budget deficit. And the Council will decide about Finland's violations.

But the key is France which enjoys, again, a compromise after the country was given three times an extension to correct its fiscal positions. Paris has time until 10 June to report on the measures the government has undertaken to implement the Council recommendation. Only then will the Commission decide whether France will be sanctioned or not. In the mean time, in the analysis that accompanies the CSRs the Commission points out that there are big risks France not to respect the fiscal provisions. These risks are much bigger than in other countries because of the size of the French economy and the possibility of negative spillovers in the entire euro area. In addition to France not being able to correct its budget deficit and its public debt is growing the country has the highest tax burden in the EU.

In 2014, the tax-to-GDP ratio was 45.9%. France also has very high social spending - 26% of GDP which is almost half of the public spending. All this in the well familiar combination of very restrictive and regulated labour market, bureaucracy and non-attractive business and investment environment. That is why the Commission CSRs are aimed precisely to these areas. Nonetheless, in the first quarter of this year France outpaced two times Germany and the growth champion Britain. The country's gross domestic product grew 0.6% in the first 3 months of the year which surpassed the expectations of the economists.

Croatia, too, avoided severe criticism, although the perspectives for the country are not very bright. Croatia as well is at great risk of non-compliance with the Stability and Growth Pact provisions. Just like with France with Croatia, too, there are some serious contradictions. On the one hand the Commission says that it will not use the stick because the national reform programmes of the two countries are ambitious but on the other hand, in the analysis attached to the recommendations, it is said that their efforts are not at all ambitious. "The level of ambition remains below expectations in a number of areas, notably as regards tightening early retirement rules and publishing and implementing the findings of the expenditure review, although some additional measures were presented to partly compensate for the shortfall", the analysis says on Croatia. The Commission hesitation to put the right assessment of the country is visible given the upcoming elections in the end of this year or the beginning of the next, but in the analysis can still be found an accurate diagnosis.

"[...] in a context of subdued growth, delayed restructuring of firms and dismal employment performance, the risks associated with weak competitiveness, large external liabilities and rising public debt coupled with weak public sector governance have increased significantly".

"[...] in a context of subdued growth, delayed restructuring of firms and dismal employment performance, the risks associated with weak competitiveness, large external liabilities and rising public debt coupled with weak public sector governance have increased significantly".

Britain is another country which gets remarkable lenience. One could even think that the Commission behaves with the United Kingdom already as if it is an alien body that nothing depends on. This was especially visible in Commissioner Moscovici's words when presenting the recommendations: "The United Kingdom did not correct its excessive deficit by the deadline set by the Council recommendation, which is an old one since 2009 and the supposed deadline was financial year 2014-15. We therefore propose a Council decision establishing non-effective action and setting a new deadline of financial year 2016-17 to bring the deficit below 3% of GDP. I don't need to recall that Great Britain is not a member of the Eurozone".

In the accompanying analysis the situation sounds better grounded. As there is no mid-term objective in Britain's national reform programme (because UK did not sign the fiscal compact), the Commission takes as starting points the current situation and the government's expectations for reduction of the deficit to 2.2% of GDP in 2016-2017. On the basis of the spring economic forecast the Commission believes the UK will be capable to comply with the SGP provisions by then. That is why it is simply adjusting the deadline to the expectations of the government in London. Given the now certain referendum on UK membership in the EU even earlier than planned, the Commission decision is understandable to avoid unnecessary conflicts with the already electrified British public opinion. However, this is a bad signal that rules can be ignored every time the Commission has an intractable government to deal with.

Poland is also getting remarkable lenience. The reason the Commission to propose the excessive deficit procedure to be suspended for Poland earlier is that, statistically, Poland corrected its deficit to below 3% last year. As Mr Moscovici explained, Poland's budget deficit was 3.2% of GDP in 2014 but Eurostat confirmed that the deficit would have been below 3% had there were not payments made related to the pension reform. In other words, the Commission is trying to apply here its interpretation of the flexibility of the EU fiscal rules. According to that interpretation, published in the beginning of the year, the countries that make significant reforms, especially of the pension system, could get favourable attitude when their budget deficit is assessed.

The problem is, though, that in its analysis on Poland the Commission points out that in the end of 2013 Poland reversed its systemic pension reform started in 1999. This, according to the Commission, gives some budgetary relief in the short term but in the longer term it is expected to have some serious consequences for the public finances. The Commission actions are odd also toward Finland. Pierre Moscovici announced on 13 May that the country is in violation of the budget deficit and the public debt rule but it decided to leave the member states to decide what to do with this country. From the Commission analysis it becomes clear that Finland will not be able to comply with the SGP requirements. "For Finland, we have prepared a report assessing Finland's breach of the debt and the deficit criterion, concluding that both criteria are not complied with (respectively 64% for debt ratio and 3.4% for deficit level in 2016). The Member States will have to assess our report and on the basis of  their conclusions we will then have to decide whether to formally propose or not to open the procedure for excessive deficit on Finland", Mr Moscovici said.

their conclusions we will then have to decide whether to formally propose or not to open the procedure for excessive deficit on Finland", Mr Moscovici said.

But, practically, everything is now in the hands of the member states. There are two scenarios for development of the situation. The first is the countries to take advantage of the favourable economic conditions and do nothing as always so far. The boomerang will return when the oil prices change or another cataclysm happens which, in the current geopolitical situation, is not unlikely. The second option is, thanks to some European miracle, the member states to suddenly decide to take the Commission recommendations as their own and start serious reforms. I would not bet any money on the latter, although in their 12 May conclusions the EU finance ministers recognise "that further structural reforms in the services, product and labour markets and responsible fiscal policies are needed in all Member States to strengthen and sustain the economic recovery, correct harmful imbalances, achieve fiscal sustainability, improve the conditions for investment and reinforce the single market, unleashing the growth potential of Member States' economies". Words sound good. When can we expect actions?

Klaus Regling | © Council of the EU

Klaus Regling | © Council of the EU Mario Centeno | © Council of the EU

Mario Centeno | © Council of the EU Mario Centeno | © Council of the EU

Mario Centeno | © Council of the EU