Cameron vs EU - 3:1

Adelina Marini, August 19, 2014

David Cameron's relations with the EU have always been based on victory or loss. In this regard, the score in the match between Great Britain and EU (the euro area in particular) is 3 to 1 for London. The British prime minister has scored three wins over his should-have-been-partners opponents. Naturally, this score is completely conditional and is based on the suggested personal feelings of Mr Cameron. His first huge victory over the EU was when he imposed a veto on the fiscal compact. At the time, he did not assess the situation well and decided in a key moment for the euro area to raise "personal" issues (affecting only the UK) as a precondition for London's support for this important piece of legislation about fiscal discipline. This has led to taking it out in a separate treaty which is to be gradually intertwined in the current EU legislation. So, practically, he both won and lost, depending on the point of view.

David Cameron's relations with the EU have always been based on victory or loss. In this regard, the score in the match between Great Britain and EU (the euro area in particular) is 3 to 1 for London. The British prime minister has scored three wins over his should-have-been-partners opponents. Naturally, this score is completely conditional and is based on the suggested personal feelings of Mr Cameron. His first huge victory over the EU was when he imposed a veto on the fiscal compact. At the time, he did not assess the situation well and decided in a key moment for the euro area to raise "personal" issues (affecting only the UK) as a precondition for London's support for this important piece of legislation about fiscal discipline. This has led to taking it out in a separate treaty which is to be gradually intertwined in the current EU legislation. So, practically, he both won and lost, depending on the point of view.

In the short-term this brought domestic dividends to the British premier, but pounded a wedge into the European Union's very heart creating a precedent - crucial issues about the future to be dealt with outside the EU instead of upgrading the Union. This experience was again applied with the second pillar of the banking union but not because of any country's resistance but because of fear that if the treaties were to be opened for repairs this would throw the Union into a severe existential crisis.

David Cameron's second victory was in the negotiations on the European budget (the multiannual financial framework 2014-2020). Again, under his peremptory pressure a nominal reduction of the Community's budget was agreed. This, too, is a short-term political win of the British prime minister with a potential huge damage in the long-term for the entire EU, which is yet to need a common fund to solve its growingly common problems.

His great loss was with the fiasco around the election of the European Commission president. It stroke a really huge blow on his ambition to win the "war" with Brussels before he had even articulated what its goals are. Now, however, the chance has smiled at him and has brought him his third and probably most significant win so far - a record high economic growth. The data about the economic performance in the EU for the second quarter show that while the German economy is shrinking (-0.2%), the UK economy is growing rapidly (+0.8%). On a year-o-year basis, the British economy has registered its best performance in six years - growth rate of 3.2%. Much better than Germany whose slowdown was predicted and is already a fact. All this against the backdrop of the frozen in weightlessness and non-reformness French economy and also of the Italian economy which has entered its third recession since 2008.

Of course, nothing is that simple as it seems when comparing statistical data, but it is more than certain that the good performance of the British economy will inject new energy in David Cameron's bellicosity, especially bearing in mind the approach of the parliamentary elections in the UK next year. And although the premier is for now reserved in his reactions on the occasion of Eurostat's latest data, it can be expected that this will be a very strong trump card in his sleeve when the new political season begins in the EU. The dynamic growth of the British economy will be an argument in David Cameron's thesis that Brussels's centralised approach has led to recession even the eurozone's powerhouse - Germany - and that the looser the links with the Union the better for the economy.

This thesis will, for sure, get broad support among the newcomers in the European Parliament, especially in the third largest political group - the European Conservatives and Reformists, part of which are also the Alternative for Germany who are slowly but steadily gaining support in Germany. The return of the crisis will certainly be a strong argument in their hands against "Brussels's bad policies", as under "Brussels" it is usually assumed the European Commission. Alas, the economic concepts are being drawn by the Commission and the member states and their implementation depends solely on the latter. In this context, the new Commission will face a significant challenge while preparing the fifth European semester, namely to analyse objectively the reasons for the uneven distribution of recovery. It is also very important the data of the British success to be interpreted correctly both in London, Brussels, Berlin, Paris or Rome.

Britain is a special case

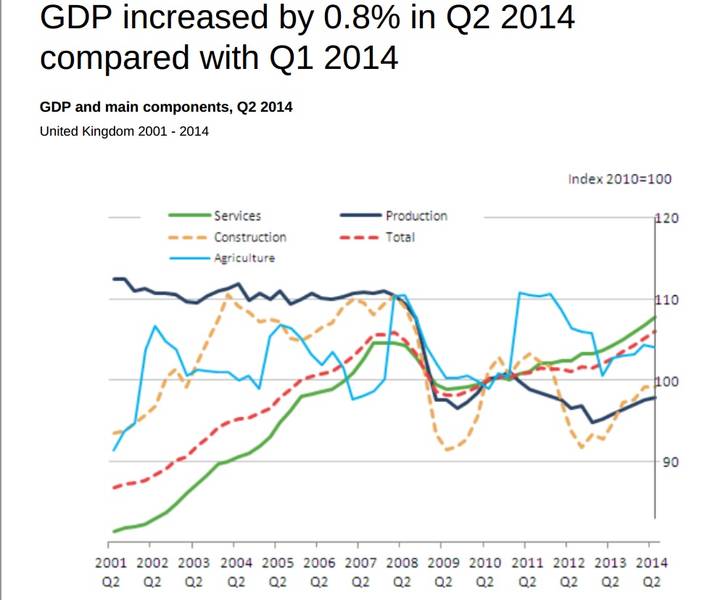

It will be very rashly to conclude that the British economy is performing well because it is farther from Brussels and the biggest euro area economies suffer because they share a common currency and are closely interlinked, because the Eurostat data clearly show that many countries in the currency block show power in terms of growth. The Baltic states are in permanent and very dynamic growth. Portugal also scored growth of 0.6% in the second quarter same as Slovakia and Spain. The Dutch economy, too, has grown in the period April-June (+0.5%). The record high economic achievements of the royal economy are mainly due to growth of services. This is the dominant sector which has grown by 1.0% in the period April-June - the fastest growth quarterly since the third quarter of 2012. The services sector has an 80% share in the British economy and is currently much bigger than the pre-crisis period. In the same time, production and construction continue to be smaller compared to pre-crisis levels and their growth curve is quite curly. In the second quarter they even dropped, as well as agriculture.

According to the European Commission, however, the United Kingdom is suffering from macro economic imbalances and is violating the Stability and Growth Pact. This is not very important from a British point of view because the relevant provisions are not mandatory for Britain and the only thing the Commission can do is to recommend. The greatest imbalances are in the housing market creating structural problems because of household debt related to high levels of mortgage debt and the structural characteristics of the housing market. The risks for the housing sector are related to the continuous lack of housing, especially in London and the slow response of supply. This is pushing housing prices high up, especially in London, and is forcing buyers to take expensive mortgages.

Last autumn, the Commission made a review of the implementation of the country-specific recommendations, including for UK, and pointed out that the country has another big problem - labour market. Although employment is still high (71.1%), the youth unemployment levels and the levels of young people not engaged in education or training are a cause of concern. Many people, especially young, are engaged in temporary or part-time work. In addition, the number of low-qualified workers is very high and there is shortage of high-quality workers with technical skills. UK is also losing on the front of productivity compared to its peers in the G7.

According to the latest data, quoted by the Commission, hourly productivity was 16% lower than the average in the Group of Seven most powerful economies in the world in 2012 and with 2% lower than its own level in 2007. Britain is among the countries with highest risk of poverty and social exclusion in the EU. Public finances are not in perfect shape as well. In its convergence programme, UK does not have a mid-term objective as is envisaged in the Stability and Growth Pact, which all the efforts of the other member states are based upon - the mid-term objective is the horizon the governments have  agreed to pursue. For 2014-2015 the programme envisages a budget deficit of 5.0% of the gross domestic product - a decline compared to the peak of 11.4% in the period 2009-2011.

agreed to pursue. For 2014-2015 the programme envisages a budget deficit of 5.0% of the gross domestic product - a decline compared to the peak of 11.4% in the period 2009-2011.

The convergence programme aims to reduce the deficit to 2.4% of GDP in 2016-2017, two years after the deadline set by the Council. The Commission has formulated, in the beginning of June, six recommendations for Britain, which are quite advisable. Among them is to correct the excessive deficit, more transparency at the housing market, reducing child poverty in low-income households, efforts to improve funding for SMEs, transparency in the implementation of the National Infrastructure Plan. On July 8 the Commission's specific recommendations have been approved as for Britain the economic and financial affairs Council (ECOFIN) points out that consolidation is still mainly based on cutting expenditure and is recommended London to consider improving the revenue side by expanding the tax base.

UK's public debt is expected to peak to 93.1% of GDP in 2015-2016 before dropping to 86.6% in 2018-19. The Council sees potential risks for the implementation of the UK budget forecasts if there is lower than expected GDP growth due to low wages and therefore low consumption. Alas, the Eurostat data reject (for now) these risks.

At first reading, it seems David Cameron is doing better than his "rivals" in the euro area. UK Treasury Secretary George Osborne pointed precisely at the euro area as the most significant risk for the growth of the British economy. On Twitter he welcomed the "good news" pointing out that this is the fastest growth in G7. The question is whether the government will use the latest data as a boost to continue its policy of tearing apart with EU or to continue to demand reforms from its partners. At this stage, there are no moods for more reforms in the Union but rather for implementation of what has already been agreed and this will be the greatest challenge for Jean-Claude Juncker, especially against the backdrop of the calls to loosen the belts.

Crucial for the tone of the new political season will be how will Germany interpret the data about its economy. The most important, however, will be to really make a sober and unbiased analysis of why Britain is succeeding in spite of its high public debt and macro economic imbalances and France, Italy and Germany do not. And should France, Italy and Germany be put in one group? And do the Baltic states succeed for the same reasons as the UK or for other reasons? It could turn out that Britain is succeeding simply because it is doing reforms not because it is far from the "centre" and then David Cameron will again be a winner but in another thesis. That is why, it is very important to do an accurate diagnostics of the situation to avoid the mistakes from the first season of the crisis when the wrong symptoms were treated.

Klaus Regling | © Council of the EU

Klaus Regling | © Council of the EU Mario Centeno | © Council of the EU

Mario Centeno | © Council of the EU Mario Centeno | © Council of the EU

Mario Centeno | © Council of the EU